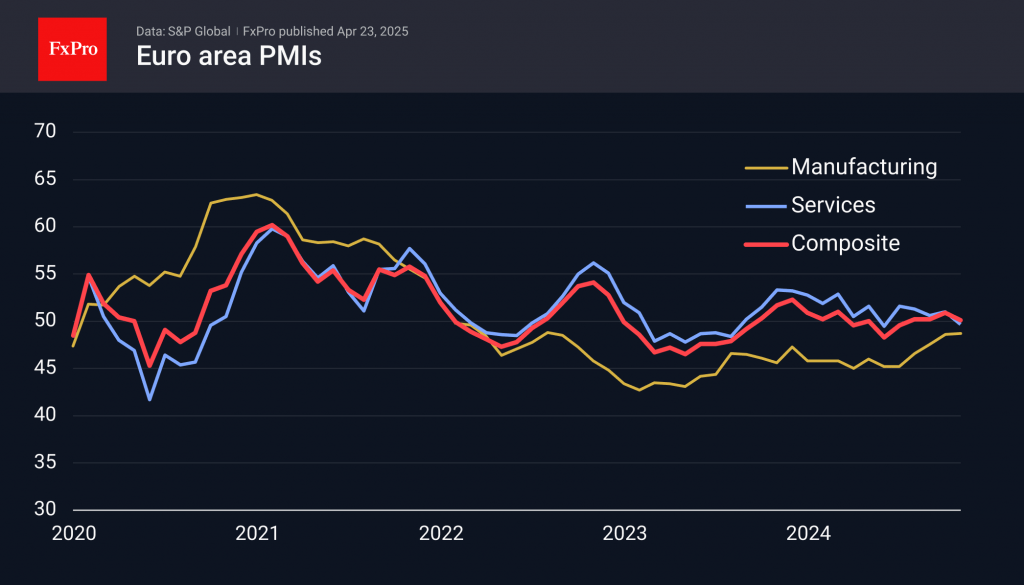

The Flash PMI estimates for the Eurozone show the complexity of the situation. Due to falling orders and falling business confidence, the composite index for the Eurozone was at 50.1 in April, struggling to cling to growth (above 50), down from 50.9 in March.

The Manufacturing PMI at 48.7 remains in contractionary territory, although its reading is the highest since January 2023 and notably above the expected 47.4. However, this upward move is threatened by the intensification of tariff wars since the start of April, which could cause a shock to the indices in the coming months.

The Service PMI also retreated below the waterline to 49.7 from 51.0 a month earlier, missing economists’ expectations of an average decline to 50.4.

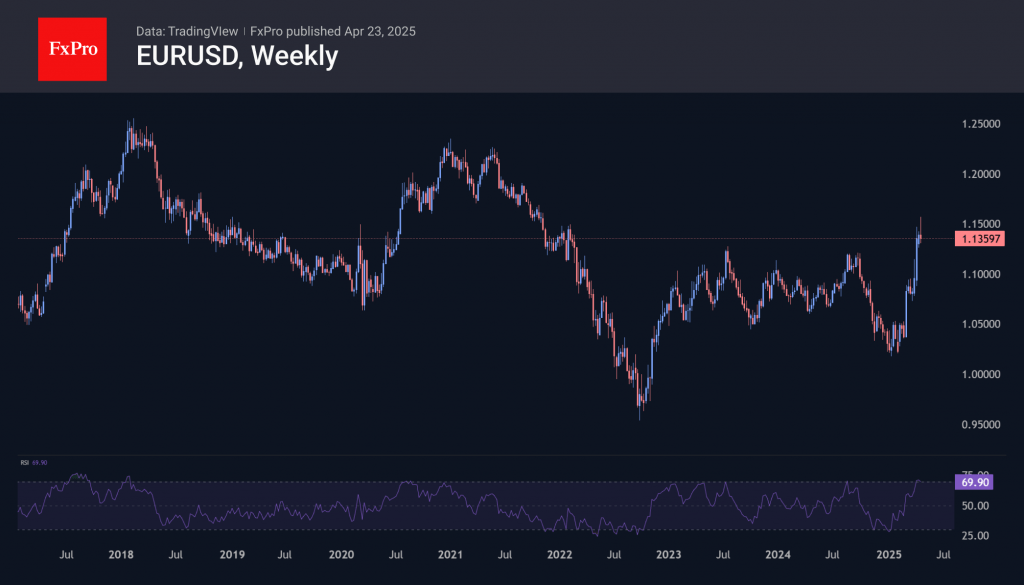

In terms of volatility potential for the euro, preliminary PMIs are the second strongest market event after ECB decisions. However, this time, the single currency faltered a bit before we saw the disappointment in the latest data. EURUSD added almost 7.5% in April to 1.1570 (a 3.5-year high) at the start of the week before it stalled and started to correct. Even before this news, the pair was approaching 1.1300, stabilising near 1.1400 at the time of writing.

Recent fluctuations in the pair have been hard to miss. On Tuesday and Wednesday, we see the dollar attempting to strengthen following Powell’s easing pressure and Trump’s invitation to China for trade talks. Historically, EURUSD has a positive correlation with stock indices, but in April, bad news for the S&P500 and Nasdaq-100 pushed up the value of gold and the euro exchange rate. This historical direct correlation is supporting EURUSD intraday on Wednesday.

The main obstacle to growth appears to be the pair’s local overbought condition at the start of the week, which has shown maximum RSI values on weekly timeframes since 2018. At such levels, there are high chances of rather painful pullbacks for short-term traders.

The FxPro Analyst Team