The Pound Sterling (GBP) faced rejection once again on its way to the 1.3500 level when compared with the US Dollar (USD), sending GBP/USD back toward the 1.3300 mark.

Pound Sterling returns to the red

GBP/USD faced a double whammy and returned to the red, reversing a major portion of the previous week’s recovery.

The pair felt the heat of the USD resurgence as a safe-haven asset, while increased dovish bets surrounding the Bank of England’s (BoE) interest rate outlook added to its downside.

Growing geopolitical and trade tensions dented risk appetite at the start of the week, lifting the haven demand for the Greenback at the expense of the higher-yielding Pound Sterling.

US President Donald Trump threatened late Monday to slap 155% tariffs on China from November 1 unless they make a deal. This came even after US Treasury Secretary Scott Bessent’s comments that he would meet with Chinese Vice Premier He Lifeng in Malaysia to de-escalate the renewed trade tensions over rare earth metals and software.

Meanwhile, the failure to end the budget deadlock between the Democrats and Republicans for the fourth consecutive week also weighed on investors’ sentiment.

Toward midweek, tensions eased on the US-China trade front as Trump touted a fair deal with China during his meeting with China’s President Xi Jinping in South Korea on October 30.

However, the relief to markets was only short-lived as risk-off flows returned after Trump imposed sanctions on Russian oil companies and accused the Russians of a lack of commitment toward ending the war in Ukraine.

Markets also digested the disappointing earnings reports from US tech giants. Tesla reported below forecast profits, while Netflix tumbled on a grim outlook.

“Apple shares fell 1.6% after the tech giant was hit with a complaint to EU antitrust regulators by two civil rights groups on Wednesday,” per Reuters.

On the UK-side of the story, the Pound Sterling extended losses after softer inflation data for September boosted bets for a BoE rate cut in December.

The Office for National Statistics (ONS) showed on Wednesday, consumer inflation held steady at 3.8% last month, defying the expected 4% growth.

“Traders rushed to price a 75% chance of the BoE cutting rates by its December meeting – up sharply from a 46% probability before the data was published – although those odds eased back to 61% on Thursday,” according to Reuters.

On Friday, the ONS reported that UK Retail Sales unexpectedly rose 0.5% over the month in September, marking a fourth consecutive monthly increase. Meanwhile, the headline S&P Global Flash UK Composite PMI registered 51.1 in October, up from 50.1 in September and above the 50.6 expected. The Pound Sterling found little inspiration from the upbeat data but failed to stage a decisive rebound.

Heading into the weekend, GBP/USD remained near the lower limit of its weekly range as investors assessed mixed macroeconomic data releases from the US. Annual inflation, as measured by the change in the Consumer Price Index, edged higher to 3% in September from 2.9% in August. This reading came in below the market expectation of 3.1%. On a positive note, S&P Global Composite PMI improved to 54.8 in October’s flash estimate from 53.9 in September.

Eyes on the Fed verdict and potential US data releases

Markets are expecting that the budget deadlock between Democrats and Republicans could end anytime soon, paving the way for the release of a string of delayed US economic data in the upcoming week.

In case the government funding is restored, the September US Nonfarm Payrolls reports will be published and will hog the limelight alongside the Fed’s October 28-29 monetary policy meeting.

A bunch of other top-tier statistics from the US will also be closely eyed for fresh hints on the Fed’s rate cut outlook.

Traders will look forward to the US Durable Goods Orders, the advance third-quarter Gross Domestic Product (GDP) and the core Personal Consumption Expenditure (PCE) Price Index.

The Fed officials will return to the rostrum on Thursday, following the end of the ‘blackout period’.

Additionally, the focus will remain on the geopolitical and trade-related headlines as Trump meets with China’s President Xi Jinping in South Korea.

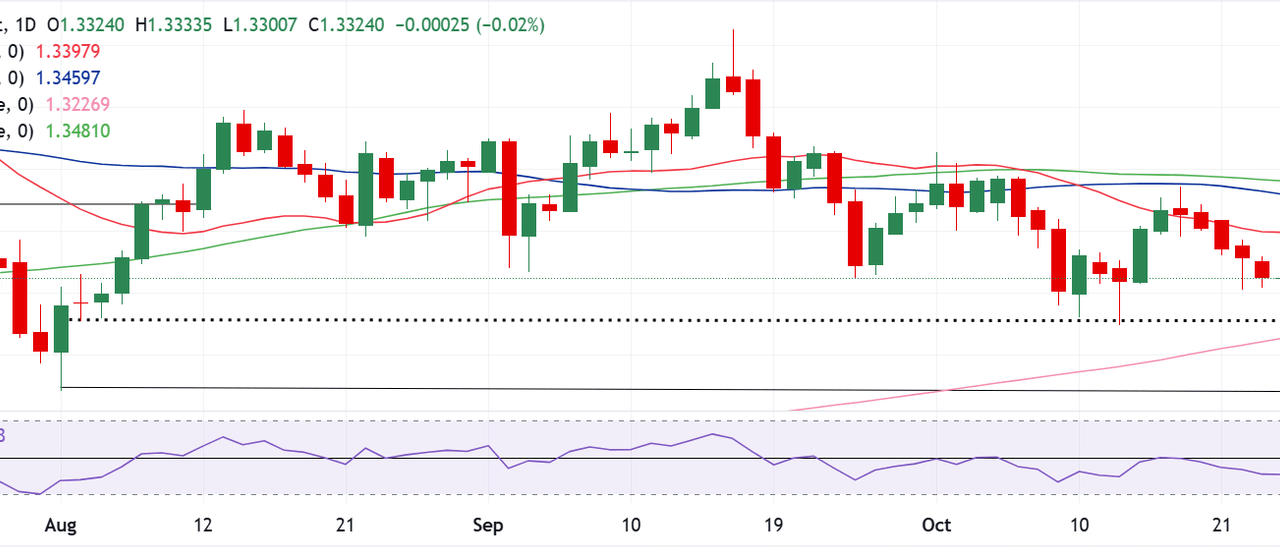

GBP/USD: Technical outlook

GBP/USD extended its reversal from near the 1.3450 region, having failed to find acceptance above the 21-day Simple Moving Average (SMA) on a daily candlestick closing basis.

If the downside gains further traction, the 1.3250 demand area could be tested, below which the immediate support is seen at the 200-day SMA at 1.3226.

A sustained break below the latter could confirm the downtrend toward the August low of 1.3142.

The 14-day Relative Strength Index (RSI) fell below the 50 level, currently near 41, suggesting that the bearish potential remains intact.

On the flip side, any recovery attempts will need to recapture the 21-day SMA support-turned-resistance, now at 1.3398.

The next relevant upside barrier is aligned at the 50-day SMA at 1.3460, followed by the 100-day SMA at 1.3481.

If the buying interest intensifies around the GBP/USD pair, the 1.3600 threshold will be a tough nut to crack.

Further north, the July 4 high of 1.3681 will come into play.

Fed FAQs

Monetary policy in the US is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability and foster full employment. Its primary tool to achieve these goals is by adjusting interest rates.

When prices are rising too quickly and inflation is above the Fed’s 2% target, it raises interest rates, increasing borrowing costs throughout the economy. This results in a stronger US Dollar (USD) as it makes the US a more attractive place for international investors to park their money.

When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates to encourage borrowing, which weighs on the Greenback.

The Federal Reserve (Fed) holds eight policy meetings a year, where the Federal Open Market Committee (FOMC) assesses economic conditions and makes monetary policy decisions.

The FOMC is attended by twelve Fed officials – the seven members of the Board of Governors, the president of the Federal Reserve Bank of New York, and four of the remaining eleven regional Reserve Bank presidents, who serve one-year terms on a rotating basis.

In extreme situations, the Federal Reserve may resort to a policy named Quantitative Easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system.

It is a non-standard policy measure used during crises or when inflation is extremely low. It was the Fed’s weapon of choice during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy high grade bonds from financial institutions. QE usually weakens the US Dollar.

Quantitative tightening (QT) is the reverse process of QE, whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing, to purchase new bonds. It is usually positive for the value of the US Dollar.