- The Pound Sterling held its corrective decline against the US Dollar amid lingering tariff concerns.

- GBP/USD traders gear up for an action-packed week ahead as trade talks and inflation data loom.

- Technically, GBP/USD appears at a critical juncture, exposed to two-way risks.

The Pound Sterling (GBP) entered a consolidative phase against the US Dollar (USD), following the recent GBP/USD correction from near four-year highs of 1.3789.

Pound Sterling continued its correction amid trade tariff jitters

Despite the corrective consolidation, GBP/USD sellers held the upper hand amid a steady recovery staged by the US Dollar from multi-year troughs.

The Greenback attracted safe-haven flows as trade war fears resurfaced, following US President Donald Trump’s announcements of new tariffs throughout the week.

Markets set off the week unnerved as Trump’s July 9 trade deal deadline approached.

Trump announced on social media on Monday that 25% tariffs will be imposed on imports from Japan and the Republic of Korea, respectively, beginning August 1.

Later, he announced that similar letters were sent to the leaders of 12 other countries, informing them that tariffs ranging 25% to 40% will be charged starting next month.

Fresh tariff headlines continued to dominate risk sentiment, boosting the go-to haven US Dollar while smashing GBP/USD to 10-day lows of 1.3526.

Heading into the Minutes of the US Federal Reserve (Fed) July meeting, Trump threatened 10% additional levies on all BRICS nations, including India, effective August 1, while also announcing 50% tariffs on Copper imports.

President Trump on Wednesday issued August 1 tariff notices to seven minor trading partners, with a 20% tariff on goods from the Philippines, 30% on goods from Sri Lanka, Algeria, Iraq, and Libya, and 25% on Brunei and Moldova.

He further announced a 50% tariff on US copper imports and a 50% duty on goods from Brazil, both effective on August 1.

Lingering trade tensions and the hawkish Fed Minutes provided further strength to the ongoing USD recovery, keeping the pair in multi-day lows.

The Minutes “showed that only “a couple” of Fed officials believed interest rate cuts could happen as early as this month, with most favouring reductions later this year,” per Reuters.

In the second half of the week, markets digested Trump’s fresh threat of a 35% tariff rate for goods imported from Canada, starting August 1.

He went on to announce more tariffs and noted he planned to impose blanket levies of 15% or 20% on most trade partners.

Late Thursday, the President said the European Union (EU) could receive a letter on tariff rates by Friday, raising doubts about the progress of trade talks between Washington and the old continent.

Risk sentiment remained sour on Friday, with GBP/USD licking its wounds and bracing for a big week ahead.

The pair was also weighed down by the unexpected UK economic contraction in May. Data from the Office for National Statistics (ONS) showed UK Gross Domestic Product (GDP) contracted 0.1% month-on-month (MoM) in May, compared to an expected 0.1% growth.

Other data from the UK showed that monthly Industrial and Manufacturing Production came in at -0.9% and -1%, respectively, in May. Both readings fell short of market expectations.

Focus on trade headlines in the US/UK inflation week

An action-packed week is unfolding, following a relatively quiet one data-wise.

However, fresh updates surrounding US President Donald Trump’s tariff plans will continue to flow, dictating market sentiment and the higher-yielding Pound Sterling.

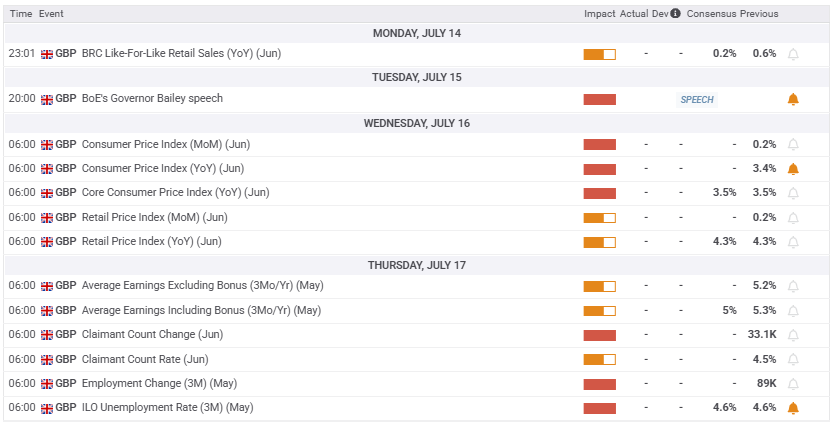

Traders brace for a quiet start, with no major data releases due on Monday.

Tuesday will feature the Chinese second-quarter Gross Domestic Product (GDP) alongside the Retail Sales and Industrial Production data.

The main event risk that day will be the US Consumer Price Index (CPI) report, which will be key to altering the markets’ pricing of the Fed rate cuts this year.

Bank of England (BoE) Governor Andrew Bailey’s speech at the Annual Mansion House Financial and Professional Services Dinner, in London, will also be closely followed late Tuesday.

On Wednesday, the UK CPI inflation data will likely steal the show ahead of the US Producer Price Index (PPI) release.

The UK labor data will be reported on Thursday, followed by the US Retail Sales and the weekly Jobless Claims statistics.

The preliminary University of Michigan (UoM) Consumer Sentiment and Inflation Expectations data will be eagerly awaited on Friday for fresh hints on the inflation and interest rates outlook.

Besides data publications, all eyes will remain on the speeches from Fed policymakers as the US central bank enters the ‘blackout period’ on Saturday before its July 29-30 monetary policy meeting.

GBP/USD: Technical Outlook

GBP/USD breached the critical previous resistance-turned-support of the February 2022 high at 1.3643 on a sustained basis on Monday, paving the way for more bearishness.

The 14-day Relative Strength Index (RSI) has pierced the midline to the downside, currently near 49, opening the door for additional declines.

However, Pound Sterling buyers find immediate strong support at the 50-day Simple Moving Average (SMA) at 1.3498.

Only a sustained move below that level could initiate a fresh downtrend toward the June 23 low of 1.3371.

Ahead of that, the static demand area at 1.3445 could offer some comfort to buyers.

The line in the sand for the pair is seen at the 100-day SMA at 1.3252.

On the other hand, scaling the immediate resistance at the 21-day SMA of 1.3595 is critical to reviving the GBP/USD rally.

The next topside hurdle is seen at the 1.3750 psychological level, above which a test of the 1.3800 round level will be inevitable.

Inflation FAQs

Inflation measures the rise in the price of a representative basket of goods and services. Headline inflation is usually expressed as a percentage change on a month-on-month (MoM) and year-on-year (YoY) basis. Core inflation excludes more volatile elements such as food and fuel which can fluctuate because of geopolitical and seasonal factors. Core inflation is the figure economists focus on and is the level targeted by central banks, which are mandated to keep inflation at a manageable level, usually around 2%.

The Consumer Price Index (CPI) measures the change in prices of a basket of goods and services over a period of time. It is usually expressed as a percentage change on a month-on-month (MoM) and year-on-year (YoY) basis. Core CPI is the figure targeted by central banks as it excludes volatile food and fuel inputs. When Core CPI rises above 2% it usually results in higher interest rates and vice versa when it falls below 2%. Since higher interest rates are positive for a currency, higher inflation usually results in a stronger currency. The opposite is true when inflation falls.

Although it may seem counter-intuitive, high inflation in a country pushes up the value of its currency and vice versa for lower inflation. This is because the central bank will normally raise interest rates to combat the higher inflation, which attract more global capital inflows from investors looking for a lucrative place to park their money.

Formerly, Gold was the asset investors turned to in times of high inflation because it preserved its value, and whilst investors will often still buy Gold for its safe-haven properties in times of extreme market turmoil, this is not the case most of the time. This is because when inflation is high, central banks will put up interest rates to combat it.

Higher interest rates are negative for Gold because they increase the opportunity-cost of holding Gold vis-a-vis an interest-bearing asset or placing the money in a cash deposit account. On the flipside, lower inflation tends to be positive for Gold as it brings interest rates down, making the bright metal a more viable investment alternative.