- The Pound Sterling extended recovery from 14-month lows of 1.2100 versus the US Dollar.

- High-impact US data and Trump’s tariff talks are to drive GBP/USD in the upcoming week.

- Technically, an impending Bear Cross cautions Pound Sterling buyers.

The Pound Sterling (GBP) extended its recovery from 14-month lows of 1.2100 against the US Dollar (USD), with GBP/USD testing offers above 1.2400.

Pound Sterling witnessed extended recovery

US President Donald Trump returned to the White House for the second term, and his tariff talks remained the primary market driver, influencing risk sentiment, the US Dollar, and eventually the high-beta currency pair – GBP/USD. The Greenback languished in monthly lows against its major rivals amid uncertainty over Trump’s tariff policy and his calls to lower interest rates and the USD.

Earlier in the week, Trump announced plans to impose tariffs on imports from Canada, Mexico, China, and the European Union, to be implemented on February 1. However, no further clarity has been provided, leaving investors losing confidence in the US currency. The 47th US President also announced that OpenAI, SoftBank, and Oracle will form a joint venture called Stargate and invest up to $500 billion in artificial intelligence (AI). This announcement boosted the tech stocks globally, diminishing the USD’s appeal as a haven.

In the second half of the week, Trump said in an interview, referring to his telephonic conversation with Chinese President Xi Jinping, he “would rather not have to use tariffs on China” if he could make a deal with Beijing over fair trade practices.

Additionally, increased bets of two rate reductions by the Fed this year kept the bearish undertone intact in the buck, allowing the GBP/USD pair to build on its previous week’s recovery from over one-year lows. In doing so, the major briefly regained 1.2400, reaching the highest level in two weeks.

Tame inflation reports for December reinforced expectations that the Fed will likely stick to its forecast of two rate cuts in 2025. Markets price in a total easing of 37 basis points (bps) from the Fed this year, with the first-rate cut not fully priced until July, per LSEG data.

The USD/JPY sell-off led by the Bank of Japan’s (BoJ) hawkish 25 bps rate hike exacerbated the pain in the Greenback. Ahead of the weekend, the mixed PMI data from the US didn’t allow the USD to gather strength against its rivals. In January’s flash estimate, S&P Global Composite PMI retreated to 52.4 from 55.4 in December.

On the UK side of the equation, the Pound Sterling drew support from a risk-friendly market environment almost throughout the week.

Further, the increase in the UK’s wage growth also aided the GBP/USD recovery even though the Unemployment Rate ticked higher to 4.4% in the quarter to November. The Office for National Statistics (ONS) said Tuesday that Average Weekly Earnings rose by 5.6% in the three months to the end of November, up from 5.2% in the three months to October.

On Friday, the seasonally adjusted S&P Global/CIPS UK Services Business Activity Index rose to 51.2 in January after recording 51.1 in December while coming in above the estimated 50.6 print. The encouraging data provided extra legs to the turnaround.

However, traders see an 84% probability that the Bank of England (BoE) will lower rates by 25 bps at its policy meeting on February 6. Amid expectations of divergent monetary policy outlooks between the Fed and the BoE, the GBP/USD upswing could remain restricted.

Market participants could also refrain from placing fresh bets on the pair heading into the key event risks next week, including the preliminary US growth number and the Fed policy announcements.

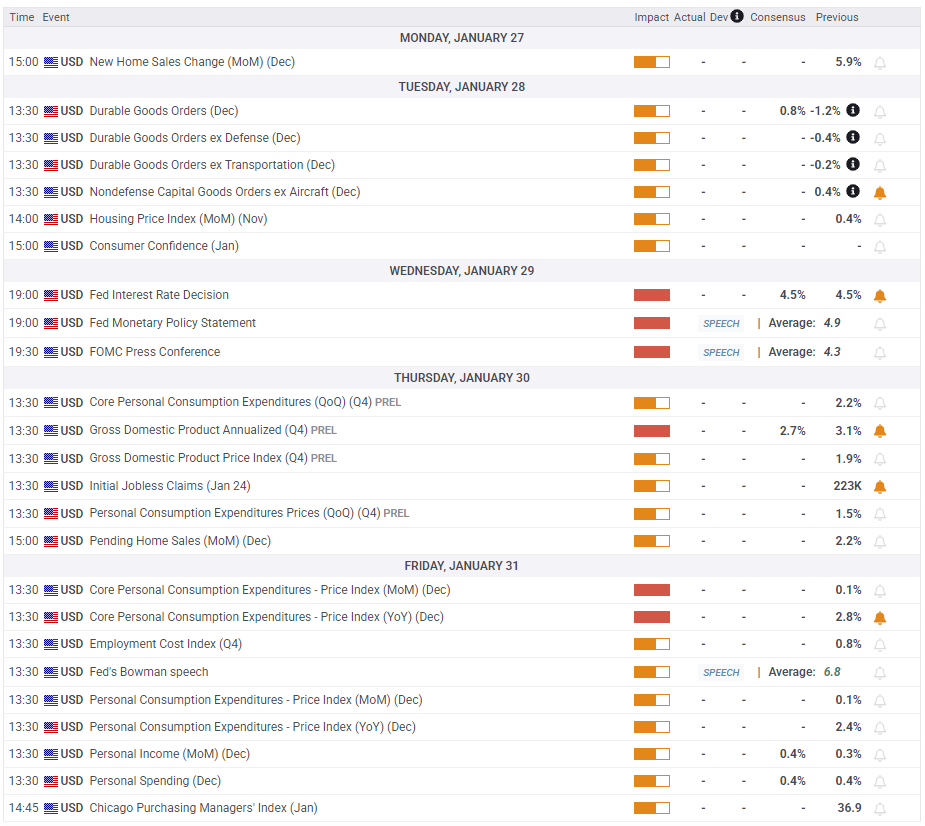

Week ahead: Top-tier US data to hog limelight

US President Donald Trump’s tariff talks and other policy announcements will continue to stir markets as traders will look to a bunch of high-impact US economic data releases for a fresh directional impetus in the GBP/USD pair.

Monday is a rather data-dry calendar on both sides of the Atlantic, but the official Chinese PMI data could impact risk-sensitive currencies such as the British Pound.

The BoE Quarterly Bulletin will be published on Tuesday, followed by the US Durable Goods Orders and Conference Board (CB) Consumer Confidence data.

On Wednesday, the Fed policy announcements will stand out, with Chairman Jerome Powell’s press conference closely scrutinized for the timing of the next interest rate cut.

Attention will then turn to the preliminary reading of US fourth-quarter Gross Domestic Product (GDP) data on Thursday. The data could infuse volatility in the USD, eventually impacting the pair.

The American calendar will also feature the weekly Jobless Claims and Pending Home Sales data on the same day.

The December US Personal Consumption Expenditure (PCE) Price Index and the quarterly Employment Cost Index (ECI) will draw close to an eventful week.

Fed policymakers will return to the rostrum on Friday as the ‘blackout period’ ends.

GBP/USD: Technical Outlook

The daily chart shows that GBP/USD buyers re-entered the six-week-long falling wedge formation to test the upper boundary of the wedge at 1.2425.

On its road to recovery, the pair recaptured the critical short-term resistance of the 21-day Simple Moving Average (SMA) at 1.2362.

However, the Pound Sterling needs a daily candlestick closing above that level to extend the recovery momentum toward the 50-day SMA at 1.2525.

Further up, the 1.2600 round level could challenge bearish commitments.

The 14-day Relative Strength Index (RSI) is set to recapture the midline, currently near 49.50. However, the 100-day SMA is on the verge of cutting the 200-day SMA from above.

A Bear Cross could be validated if the 100-day SMA pierces through the latter to the downside on a daily closing basis.

In such a case, Pound Sterling sellers could fight back control, dragging the pair back toward the wedge support at 1.2211.

Failure to defend the latter will likely expose the downside toward the previous week’s low of 1.2160.

A sustained break below that level will call for a retest of the 14-month low at 1.2100.

Fed FAQs

Monetary policy in the US is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability and foster full employment. Its primary tool to achieve these goals is by adjusting interest rates. When prices are rising too quickly and inflation is above the Fed’s 2% target, it raises interest rates, increasing borrowing costs throughout the economy. This results in a stronger US Dollar (USD) as it makes the US a more attractive place for international investors to park their money. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates to encourage borrowing, which weighs on the Greenback.

The Federal Reserve (Fed) holds eight policy meetings a year, where the Federal Open Market Committee (FOMC) assesses economic conditions and makes monetary policy decisions. The FOMC is attended by twelve Fed officials – the seven members of the Board of Governors, the president of the Federal Reserve Bank of New York, and four of the remaining eleven regional Reserve Bank presidents, who serve one-year terms on a rotating basis.

In extreme situations, the Federal Reserve may resort to a policy named Quantitative Easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system. It is a non-standard policy measure used during crises or when inflation is extremely low. It was the Fed’s weapon of choice during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy high grade bonds from financial institutions. QE usually weakens the US Dollar.

Quantitative tightening (QT) is the reverse process of QE, whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing, to purchase new bonds. It is usually positive for the value of the US Dollar.