Against a backdrop of persistent inflation and growing uncertainty about the viability of Social Security, more and more Americans are looking to regain control of their financial future.

Among the tools at their disposal, Individual Retirement Accounts (IRAs) occupy a prime position. These individual retirement accounts not only help build capital for the years to come, but also offer considerable tax advantages, which are often underestimated.

The promise is to reduce taxes while preparing for retirement, provided you understand how these schemes work and use them wisely.

Retirement accounts with a dual vocation: Savings and tax optimization

An IRA is first and foremost a long-term investment vehicle designed to finance retirement. It allows you to invest your savings in a wide range of assets, including stocks, bonds, mutual funds, etc., while benefiting from tax advantages.

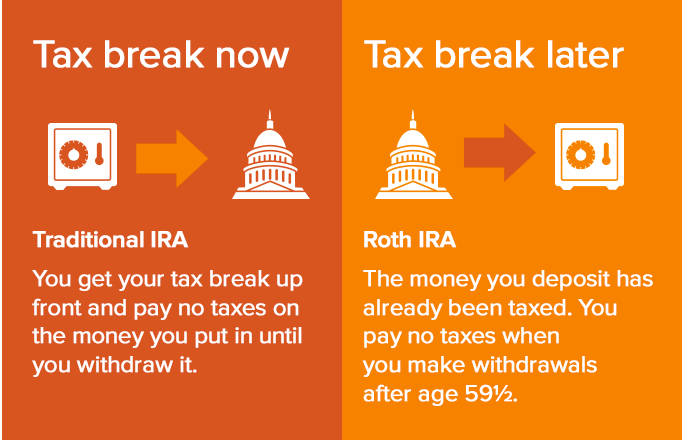

There are several variations, but the two main types are the Traditional IRA and the Roth IRA. The former offers an immediate tax deduction, subject to certain limits and depending on your income. The second, on the other hand, does not allow you to deduct the sums paid in, but guarantees tax-free withdrawals at retirement.

Source: Alliance Wealth Advisors

In both cases, capital gains, dividends and interest generated by investments are not subject to tax for as long as they remain in the account, which encourages faster capital accumulation through compounding.

The Traditional IRA: Immediate leverage to reduce taxes

The main advantage of the Traditional IRA is that contributions can be deducted from taxable income, which automatically reduces the amount of tax payable.

In 2025, the maximum contribution allowed is set at $7,000 per year for those under 50, and $8,000 for those aged 50 and over, as part of catch-up contributions.

In practical terms, a taxpayer who contributes $7,000 to a Traditional IRA will be able to reduce his or her taxable income by the same amount.

For a person with a marginal tax rate of 22%, this would save more than $1,500 in taxes over the year. This deduction is called “above-the-line”, meaning that it applies even if the taxpayer does not itemize his or her deductions.

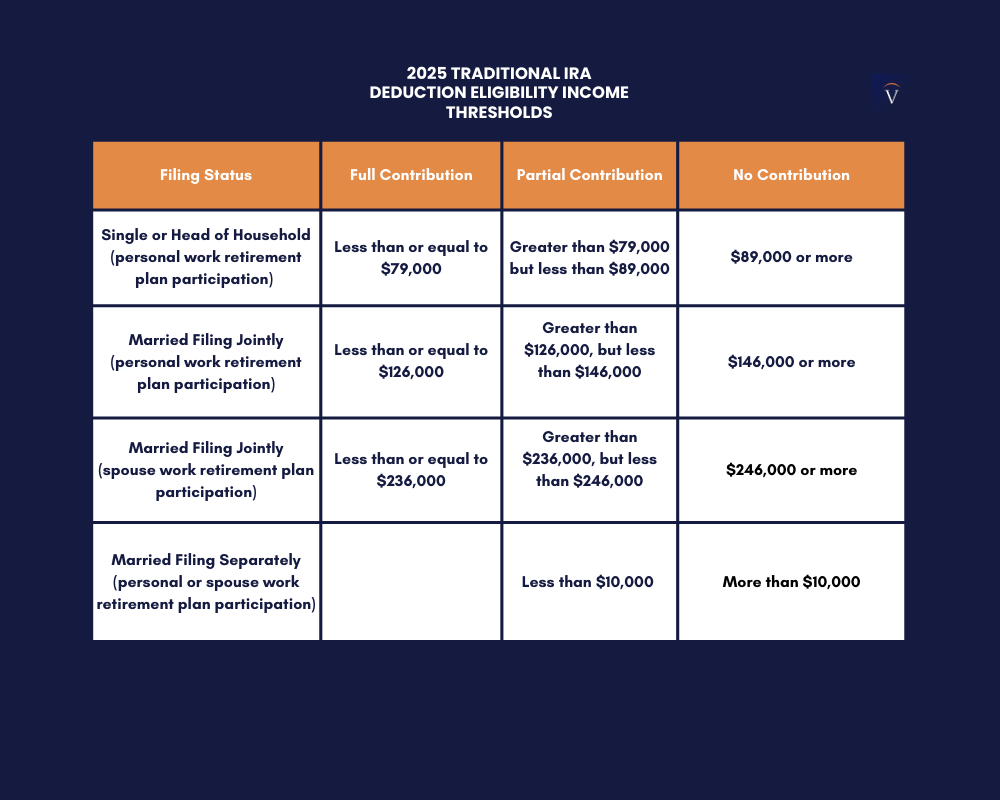

However, this benefit is not automatic. It depends on two factors: income level and participation in a company pension plan.

If the taxpayer, or his or her spouse, benefits from a plan such as a 401(k), deductions are subject to thresholds.

For example, for a single individual covered by a company plan, the deduction is full if modified adjusted gross income (MAGI) is less than $79,000, partial up to $89,000, and totally eliminated above that.

For married couples in the same situation, the deduction begins to be reduced at $126,000 MAGI and disappears at $146,000.

On the other hand, if neither has a business plan, the deduction is full, regardless of the level of income.

Source: Vision Retirement

The Roth IRA: Reverse taxation for years to come

In contrast to the Traditional IRA, the Roth IRA operates on a tax-deferred basis.

Amounts paid in are not immediately deductible, but in return, invested funds grow tax-free, and withdrawals made at retirement are totally tax-free, subject to certain conditions.

In particular, the account must have been open for at least five years, and the account holder must have reached the age of 59 and a half.

The Roth IRA offers several notable advantages. In particular, it avoids Mandatory Minimum Distributions (RMDs), which apply to Traditional IRAs from age 73. This offers greater flexibility in managing withdrawals and facilitates inheritance.

What’s more, contributions, but not earnings, can be withdrawn at any time, without penalty or tax, lending a degree of liquidity to the scheme.

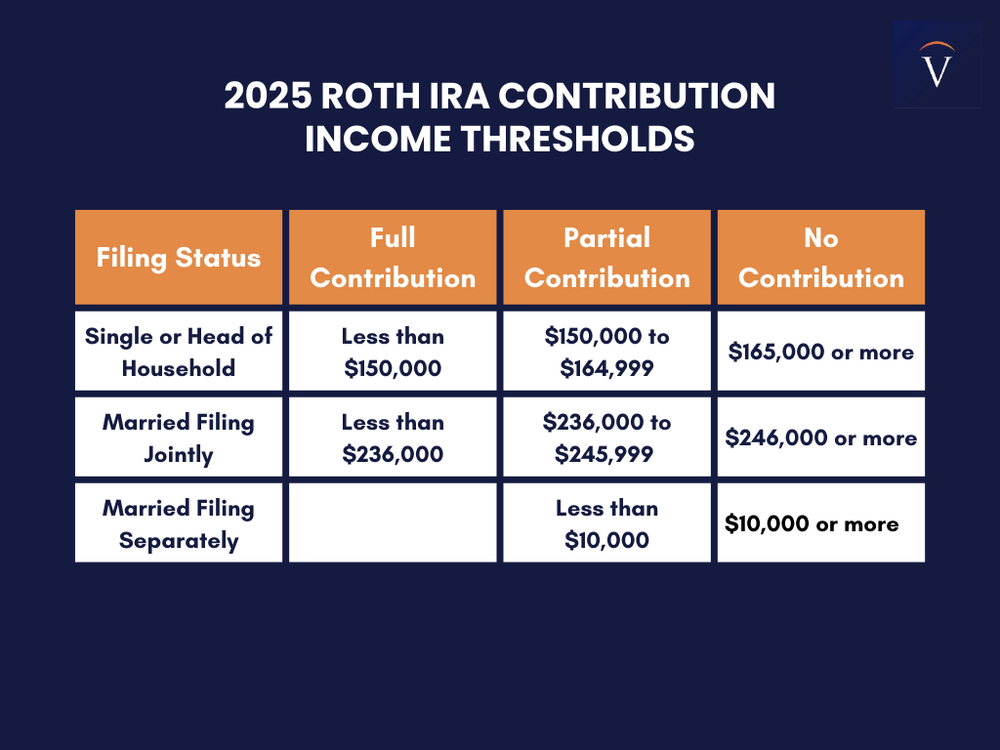

However, access to the Roth IRA is subject to income conditions. In 2025, a single person whose MAGI exceeds $165,000 will no longer be able to contribute. For married couples, the limit is $246,000. Below these ceilings, progressive reduction phases apply.

Source: Vision Retirement

Which strategy to adopt depending on your tax situation?

The choice between Traditional IRA and Roth IRA depends largely on your current tax situation and your expectations for the future.

If you’re in a high tax bracket today, but anticipate a more modest income in retirement, the Traditional IRA allows you to take advantage of an immediate deduction and defer taxation until later, when your marginal rate is likely to be lower.

Conversely, if you’re currently taxed at a low rate, but anticipate a future increase in income or taxes, the Roth IRA is a more advantageous solution, capitalizing on the exemption on withdrawals.

Some investors choose to open both types of account to diversify their tax exposure. This approach better spreads the risks associated with changing tax scales, and offers greater flexibility when it comes to withdrawing funds.

However, contribution limits are common and set at $7,000 in 2025, or $8,000 for those aged 50 and over. It is not possible to accumulate these amounts for several accounts. A taxpayer who holds both a Roth IRA and a Traditional IRA cannot contribute more than the authorized aggregate limit.

An under-exploited tax strategy

All too often overlooked, IRAs are an effective tax optimization tool for the average taxpayer.

They offer immediate leverage to lower taxable income or, conversely, the prospect of total exemption for long-term withdrawals.

Income generated in these accounts is not taxed year after year, allowing you to benefit fully from the snowball effect of compound interest.

There’s also an indirect benefit. By reducing taxable income, contributions to a Traditional IRA can also make the taxpayer eligible for other tax credits.

Retirement savings and tax optimization

Individual Retirement Accounts offer much more than just a framework for retirement savings. They offer immediate tax relief, tax-sheltered growth and flexible long-term capital management.

In an increasingly uncertain tax environment, they represent a strategic opportunity to prepare for the future.

IRAs FAQs

An IRA (Individual Retirement Account) allows you to make tax-deferred investments to save money and provide financial security when you retire. There are different types of IRAs, the most common being a traditional one – in which contributions may be tax-deductible – and a Roth IRA, a personal savings plan where contributions are not tax deductible but earnings and withdrawals may be tax-free. When you add money to your IRA, this can be invested in a wide range of financial products, usually a portfolio based on bonds, stocks and mutual funds.

Yes. For conventional IRAs, one can get exposure to Gold by investing in Gold-focused securities, such as ETFs. In the case of a self-directed IRA (SDIRA), which offers the possibility of investing in alternative assets, Gold and precious metals are available. In such cases, the investment is based on holding physical Gold (or any other precious metals like Silver, Platinum or Palladium). When investing in a Gold IRA, you don’t keep the physical metal, but a custodian entity does.

They are different products, both designed to help individuals save for retirement. The 401(k) is sponsored by employers and is built by deducting contributions directly from the paycheck, which are usually matched by the employer. Decisions on investment are very limited. An IRA, meanwhile, is a plan that an individual opens with a financial institution and offers more investment options. Both systems are quite similar in terms of taxation as contributions are either made pre-tax or are tax-deductible. You don’t have to choose one or the other: even if you have a 401(k) plan, you may be able to put extra money aside in an IRA

The US Internal Revenue Service (IRS) doesn’t specifically give any requirements regarding minimum contributions to start and deposit in an IRA (it does, however, for conversions and withdrawals). Still, some brokers may require a minimum amount depending on the funds you would like to invest in. On the other hand, the IRS establishes a maximum amount that an individual can contribute to their IRA each year.

Investment volatility is an inherent risk to any portfolio, including an IRA. The more traditional IRAs – based on a portfolio made of stocks, bonds, or mutual funds – is subject to market fluctuations and can lead to potential losses over time. Having said that, IRAs are long-term investments (even over decades), and markets tend to rise beyond short-term corrections. Still, every investor should consider their risk tolerance and choose a portfolio that suits it. Stocks tend to be more volatile than bonds, and assets available in certain self-directed IRAs, such as precious metals or cryptocurrencies, can face extremely high volatility. Diversifying your IRA investments across asset classes, sectors and geographic regions is one way to protect it against market fluctuations that could threaten its health.