The EURUSD is coming off the highest level in over 2 weeks ahead of the ECB decision at 8:15 AM ET. The expectation is for no change in policy after 7 straight meetings of declines and 8 cuts overall that has taken the main financing rate from 4.5% to 2.15%. The GBPUSD is also lower after Service PMI missed expectations but Manufacturing PMI was a slight beat, but below the 50.0 level. The USDJPY is higher after falling in the Asian session toward the 50% midpoint and finding support buyers.

In the video above, I take a look at each of those currencies from a technical perspective and outline the key levels in play.

After the US/Japan trade deal yesterday which saw Japan agreeing to a 15% tariff, and other investment pledges, the focus is back on China and EU. President Trump stated that the U.S. will implement straightforward tariffs ranging from 15% to 50% on most countries, but noted that those willing to open their markets to U.S. businesses could be offered lower rates. He highlighted ongoing efforts to finalize a trade deal with China, energy agreements with several Asian nations, and confirmed a recent deal with the EU related to military equipment. Trump also emphasized that serious discussions with the EU on broader trade issues are underway.

Meanwhile, a spokesperson for the European Union confirmed that the bloc continues to engage intensively with the U.S. on tariff negotiations. The EU is focused on reaching a negotiated solution and believes a resolution is within reach. While the EU has no intention of introducing additional countermeasures before August 1st, it remains prepared for all potential scenarios, signaling both a cooperative stance and strategic caution.

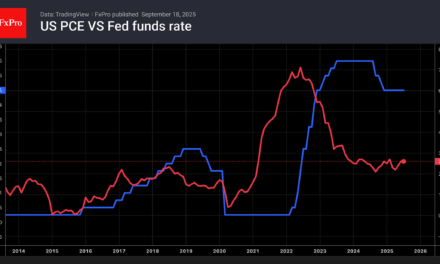

In other central bank news, the Reserve Bank of Australia (RBA) left its cash rate unchanged at 3.85% in July, despite market expectations for a 25 basis point cut. According to the meeting minutes, the board agreed that further rate cuts are warranted over time, but emphasized that the timing and extent of such easing must be carefully considered. The majority of members preferred to wait for more definitive evidence that inflation is sustainably slowing, arguing that cutting rates three times within four meetings would not align with a “cautious and gradual” approach. They also pointed to slightly firmer-than-expected inflation data and a labor market that had not softened as anticipated, reducing the urgency to cut.

A minority on the board supported a cut, highlighting downside risks to the economic outlook and noting that inflation appeared to be on track—or even below—the RBA’s target midpoint. They also warned that U.S. tariffs pose a drag on global growth, which could further weigh on Australia’s already subdued GDP. Overall, while the minutes reinforce an easing bias, they reflect a data-dependent approach and a board that remains cautious about acting too quickly, especially amid ongoing global uncertainty.

Following up to the minutes, RBA Governor Michele Bullock reiterated a measured and gradual approach to monetary policy easing, reinforcing the central bank’s cautious stance. She noted that while the labor market has eased, the adjustment has been modest, with the June unemployment rise aligning with forecasts and not seen as alarming. Other labor indicators, including vacancy rates and hours worked, remain stable, suggesting a balanced labor market rather than one facing rapid deterioration. Bullock emphasized that the RBA is not targeting a specific unemployment rate or job losses.

On inflation, Bullock warned that Q2 core inflation may not have slowed as much as initially expected, signaling potential stickiness in underlying price pressures. She stated that more data is needed to confirm that inflation is moving sustainably toward the RBA’s 2.5% target. While the risk of a severe global trade shock appears to have diminished, global uncertainty persists.

Her remarks, including those in a subsequent Q&A, downplayed the predictive power of volatile monthly job figures and affirmed the board’s decision-making wouldn’t have changed. She also mentioned that the new monthly CPI data will take time to fully integrate but will enhance inflation tracking over time. Overall, Bullock’s comments reinforce a patient and data-dependent path for rate cuts, likely tempering near-term market expectations for aggressive easing.

Overall, both the RBA minutes and Bullock signal a cautious easing bias, but Bullock was more reserved, especially regarding core inflation trends. Her emphasis on needing further confirmation before easing may temper expectations more than the minutes alone.

The PMI data in Europe was mixed:

France:

-

Manufacturing PMI: 48.4 (vs 48.5 forecast, 48.1 previous) — slightly below forecast

-

Services PMI: 49.7 (vs 49.7 forecast, 49.6 previous) — in line with forecast

Germany:

-

Manufacturing PMI: 49.2 (vs 49.4 forecast, 49.0 previous) — below forecast

-

Services PMI: 50.1 (vs 50.0 forecast, 49.7 previous) — above forecast

Eurozone (aggregate):

-

Manufacturing PMI: 49.8 (vs 49.7 forecast, 49.5 previous) — above forecast

-

Services PMI: 51.2 (vs 50.6 forecast, 50.5 previous) — beat expectations

United Kingdom:

-

Manufacturing PMI: 48.2 (vs 47.9 forecast, 47.7 previous) — beat expectations

-

Services PMI: 51.2 (vs 52.8 forecast, 52.8 previous) — significantly missed

In Asian/Pacific:

Japan:

-

Composite PMI: 51.5 (vs 51.5 previous) — unchanged

-

Services PMI: 53.5 (vs 51.7 previous) — strong improvement

-

Manufacturing PMI: 48.8 (vs 50.1 previous) — fell back into contraction

Australia:

-

Composite PMI: 53.6 (vs 51.6 previous) — notable improvement

-

Manufacturing PMI: 51.6 (vs 50.6 previous) — moved further into expansion

-

Services PMI: 53.8 (vs 51.8 previous) — solid gain

US stocks are mixed:

- Dow industrial average -192 points

- NASDAQ index up 69.34 points

- S&P index up 8 points

in Europe major indices are mixed:

- German DAX +0.37%

- France’s CAC -0.04%

- UK’s FTSE 100 +0.95%

- Spain’s Ibex +1.67%

- Italy’s FTSE MIB -0.27%

In the US debt market, yields are higher:

- 2-year yield 3.901%, +1.7 basis points

- 5 year 3.960%, +2.3 basis points

- 10 year 4.411%, +2.4 basis points

- 30 year 4.967%, +1.9 basis points

in other markets

- Crude oil is up $0.35 at $65.60

- Gold is down $25 or -0.74% at $3363.31

- Bitcoin is little changed at $118,640.

This article was written by Greg Michalowski at investinglive.com.

Source link